Is gold a good hedge against inflation?

Investors and consumers have spent the past two months inundated with news about resurging inflation. Any investor playbook worth its salt would almost instantaneously overweight gold in times of higher inflation. In theory, this should work. Inflation is supposed to be a consequence of excess money in the economy. People have more to spend, demand is higher and, with supply unchanged, prices go up. The antidote to excessive money is higher rates, which curb lending and restrict money creation. Until the new equilibrium takes place, consumers, the theory says, should rely on a more tangible asset to maintain wealth.

Throughout history, humanity has experimented with many tangible stores of wealth. From livestock and land to more exotic forms of ‘money’ such as knives (Zhou China), dolphin teeth (Solomon Islands), salt (Roman Empire), squirrel pelts (Russia) and seashells (North America). Desperate from the hyper-inflation in the early 1920’s, Germans used actual wooden money called ‘Notgelds’. However, since the Palaeolithic period, c 40,000 BC, 33 millennia before the appearance of the first cities, no asset has been a more reliable store of wealth than gold.

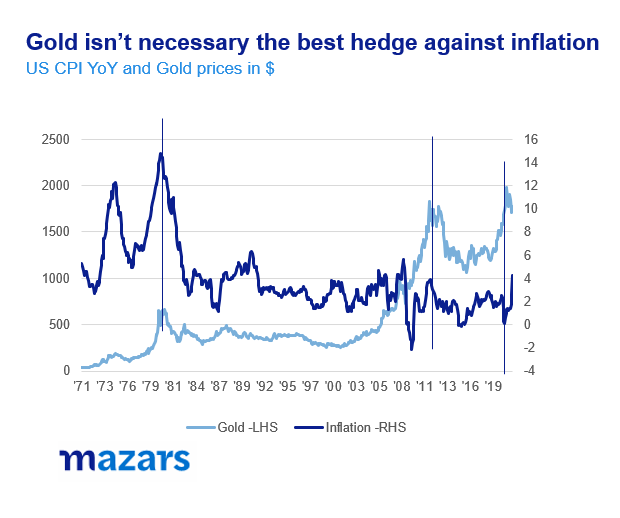

The problem with gold is that experience does not necessarily support theory. A quick look at the numbers suggests that although gold is widely perceived as an inflation hedge, reality suggests otherwise. In quiet inflationary periods gold prices rise and fall as a result of other fundamentals, such as central bank behaviour, investor and consumer demand. Additionally, its historical patterns were unequivocally affected after the introduction of Gold ETFs in the early ‘00s which made it more accessible to everyday investors who can now buy it without having to pay the transaction costs associated with buying gold from central banks or directly from exchanges.

A simple calculation from 1971 suggests a very small positive correlation (13%) between returns of gold and changes in US inflation. From 1986 to 1990, US consumer inflation rose from 1.1% to 6.3%. In the same period, gold lost 4% of its value.

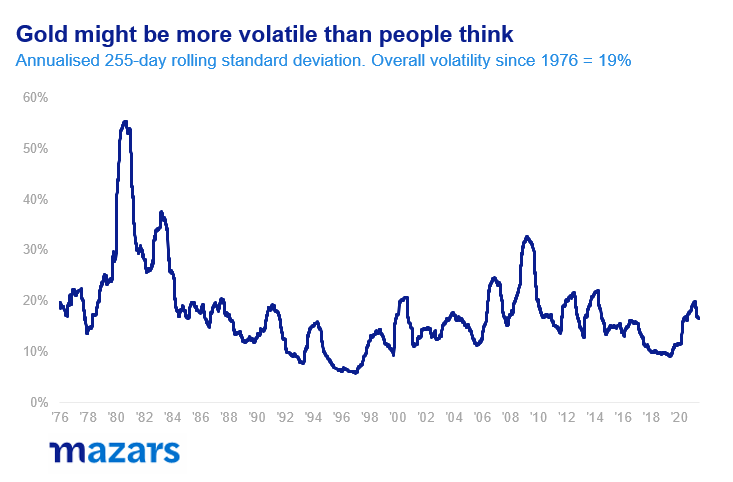

Its volatility may also surprise some investors. Annualised rolling 255-day standard deviation (a common measure of volatility) since 1976 is 19%, above that of equities (13%) and bonds (around 5%-7%).

Having said that, correlations between gold and inflation tend to increase sharply in more acute inflationary episodes, like in 1981 and 2011. Does 2021 qualify as such an episode? We believe so, as numbers suggest the highest inflation figures in a decade with some uncertainty going forward as to whether it will continue.

Investors, however, should be mindful that while correlation increases during the acute phase, it tends to decrease dramatically as inflation decelerates. Currently, central banks are not expecting a long-term bout of inflation. By historical standards this could mean some de-correlation soon.

In terms of inflation, gold can be a good trade if someone predicts inflation in advance. However, buying and holding after the event may not be as successful.

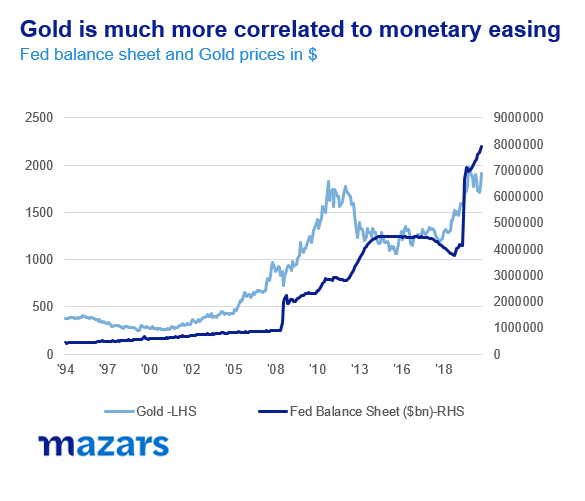

If anything, gold has proven itself to be a more effective hedge against the enormous sums being printed by central banks in reason times. The correlation between gold prices and the size of the Fed’s balance sheet is nearly 87%.

Gold prices involve central bank demand, quirky consumer preferences which different around the globe, speculation and investment heuristics. Instead of trying to time this extremely complex market with many different players, investors should consider gold as part of a wider long-term portfolio, to take advantage of all the reasons other would buy it and to protect some of their assets against unexpected changes in the inflation expectations of others.

Ding-a-ling. Financial Santa is in the house, but does he also bring rate cuts?

Unlike the real Santa, who brings his gifts late in the year, the Financial Santa, tends to begin a couple of months earlier.

Don’t write off 2023 just yet

After 2022, the annus horribilis, it was widely assumed that 2023 would be a rebound year. However, up to the end of October, a 60/40 (MSCI World/Bloomberg Barclays Global Bond Index), was up a mere 2%, very far from the average uplift of 5% and 9% experienced in a rebound year.

No end in sight

Last Friday, UK GDP came in a tick higher than expected. In this case, a 0.2% surprise is by no means insignificant. The fact that the economy was able to eke out growth in the face of already aggressive interest rate hikes will galvanise the Bank of England’s zeal to continue tightening monetary policy.

Know when to take risks, and when not to

‘Providence protect idiots’ Otto Von Bismarck once exclaimed. I’m never quite sure what the direct intentions of the Almighty are. Bismarck, a Prussian Prince and one of the great leaders of the 19th century, might have had a more direct line of communication with the powers that be than I do.

All quiet on the Western Front. Perhaps too quiet.

It was an undeniably good week for markets. US equities rose, breaking their ceiling, which held from September. This was down to two simple reasons: The closing in of a debt ceiling deal and a perhaps slightly more dovish Fed.

Weekly Market Update: War Drives Market Sentiment

US stocks started the week strongly as reports appeared to show that a ceasefire deal, in which Ukraine would abandon its drive for NATO membership in exchange for security guarantees and potential EU membership, could be possible. However, the mood soured in the middle of the week as Pentagon officials cast doubts on reports that Russia was scaling back operations in Kyiv. Nevertheless, major indices in developed markets ended higher at the end of the week, with the US stock market ending +0.7% higher, the UK stock market rising +0.8%, and European stocks gaining +2.4% in Sterling terms. Emerging markets also fared well, despite China imposing large scale lockdowns on Shanghai and showing weakening manufacturing data, as investors appear to expect that Beijing will take measures to support the economy and financial markets. UK and US bond yields retreated, ending the week at 1.61% (down 8.4 bps) and 2.39% (down 9.8 bps) respectively. Oil fell by -13.9% as Joe Biden ordered the release of 180 million barrels of crude oil from the US Strategic Petroleum Reserve, ending the week at just under $100 per barrel.

Weekly Market Update: Ukraine Tensions Continue to Unnerve Markets

Markets were whipsawed last week as traders scrambled to interpret manage the risk of conflict in Ukraine on top of newly released minutes from the Federal Reserve’s most recent meeting. How have markets reacted? Find out here...

Monthly Market Update: She is tossed in the waves, but does not sink

A hawkish Fed has sent volatility spiking, marking one of the most memorable weeks in forty years. On average, for the past five days the S&P 500’s gap between the day’s highs and the day’s lows hit 3.4%. Since 1982, only 2% of all five-day periods have been more volatile. The most important thing for […]

Weekly Market Update: Bonds Fall as Investors Escalate Rate-Hike Expectations

Market Update Equity markets posted overall gains last week after another volatile session. US stocks rose by 0.5% in GBP terms on rising energy prices, and a generally strong earnings season in which 76% of companies beat expectations. Earnings of mega-cap names had a large impact on the wider US equity market, as a 26.4% […]

Weekly Market Update: Global Stocks Fall Sharply As Geopolitical Tensions Mount

Market Update: US stocks fell by -5% last week in their worst 7-day decline since March of 2020, as fears of interest rate rises and increased geopolitical tensions weighed heavily on investor sentiment. Technology stocks in the US were hit particularly hard, falling into correction territory after having reached all time highs several weeks ago. […]

Monthly Market Update: Can the Fed be the answer to everything?

For a long time our central theme has been the disconnect between the real and the financial economy. Nowhere has this disconnect been mademore clear than in the Fed’s communication in August. The bullish economic outlook clashed directly with a dovish approach on interest rates.Actions speak louder than words, however, and it is becoming apparent […]

You can relax. The Fed has no intention to fight inflation (yet).

With inflation pressures coming mostly from the supply side, there is little the Fed can do to curb it. Interest rates are tools best used to cool down the economy during a mature, credit-driven economic boom. They are not designed for a recovering economy and much less for one still under the threat of a pandemic.

Quarterly Investment Newsletter: Summer 2021

Developed markets’ continued vaccine rollouts and a corresponding easing of lockdown measures buoyed equity markets during the second quarter despite already starting the period at elevated levels. Global stock markets rose by over +6% in Sterling terms and whilst the US was again the best performing region, European and UK stocks were not far behind. […]

The latest position of the ECB

Christine Lagarde, President of the ECB, gave a press conference on 10 June following a meeting of the ECB’s governing council. Her speech contained some unequivocally positive observations about the European economy, lamenting a bounce back in services activity, continued strong manufacturing activity and improving consumer spending, all against a backdrop of strong global demand. […]

Weekly Market Update: Markets Provide Contrasting Inflation Signals

Market Update It was a steadily positive week for equity markets last week, with all major regions gaining in Sterling terms. Emerging markets equities were the strongest performing, up +1.8%, while Yen strength saw Japanese equities returning +1.2%. Energy was the strongest performing sector globally, as oil prices reached their highest level in two years. […]

Microsoft Teams User Guide

Please access the user guide for Microsoft Teams here . User Guide – MS Teams All Mazars staff are currently working remotely due to social distancing. Given the importance of face to face contact we are now implementing face to face meetings virtually through Microsoft Teams. Please use this guide to assist you in using […]

Weekly Market Update: Stock gains muted despite signs of a trade deal

Global equities were positive last week, however energy stocks fell precipitously on plummeting oil prices, so that overall in local terms returns were +0.8%. Positive sentiment was boosted as the off-again, on-again negotiations between the US and China appear to be on-again, while a revised estimate of Q3 GDP showed the US economy expanded at […]

Monthly Market Update: New Equity Highs as Economies Tread Water

Markets welcomed signs of an easing in geopolitical tensions in October, with risk assets generally outperforming traditional safe havens. The US and Chinese authorities moved closer to agreeing a partial deal on trade, while the UK once again edged back from the precipice of a no-deal Brexit. Global central banks reiterated their dovish stances and […]

Weekly Market Update: Global Equities Rise, but Sterling Rallies More

Market Update Global stocks rose +0.7% in local currency terms, which translated into a -0.4% fall in Sterling terms. Returns were mixed in local terms, however were universally down in Sterling term as the currency rose +1.0% vs the US Dollar to just short of the $1.30 mark. Emerging Markets had a challenging week falling […]

Weekly Market Update: Bond yields rise, Pound rallies on potential Brexit “pathway”

Read our full Market Update Week 40 Global stocks gained throughout the week in local terms, however they fell in Sterling terms after the Pound rallied on news of a potential “pathway” to a Brexit deal. Global stocks fell -1.5% in Sterling terms, with the decline led by weak performance from US and Japanese equities; […]

Comments